Why are prices so high? Blame the supply chain – and that’s the reason inflation is here to stay

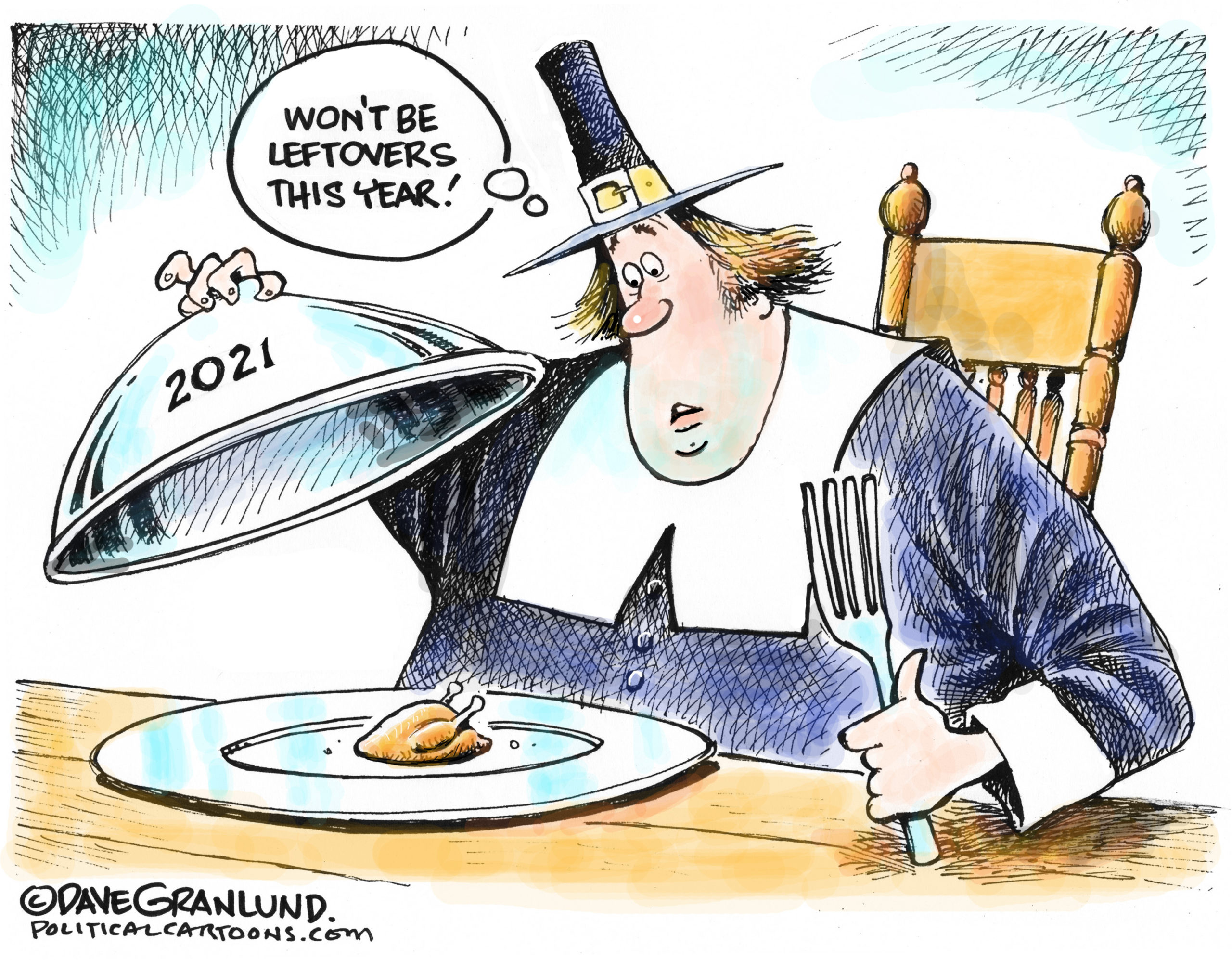

Consumer prices soared in October 2021 and are now up 6.2% from a year earlier – higher than most economists’ estimates and the fastest increase in more than three decades. At this point, that may be no surprise to most Americans, who are seeing higher prices while shopping for shoes and steaks, dining at restaurants and pumping fuel in their cars.

One of the big debates going on right now among economists, government officials like Treasury Secretary Janet Yellen and other observers is whether these soaring costs are transitory or permanent.

The Federal Reserve, which would be responsible for fighting inflation if it stays too high for too long, insisted again on Nov. 3, 2021, that it’ll be temporary, in large part because it’s tied to the supply chain mess bedeviling economies, companies and consumers.

Brooklyn Boro

View MoreNew York City’s most populous borough, Brooklyn, is home to nearly 2.6 million residents. If Brooklyn were an independent city it would be the fourth largest city in the United States. While Brooklyn has become the epitome of ‘cool and hip’ in recent years, for those that were born here, raised families here and improved communities over the years, Brooklyn has never been ‘uncool’.